Klear, Inc.

2021 Fillmore Street

San Francisco, CA 94115

+1 (415) 599-7554

Working capital is typically defined as the difference between current assets and current liabilities (current assets - current liabilities = working capital). Whilst this is technically correct and simple to understand, it does not provide the whole picture of the significance of working capital and what it truly means.

For a scaling company, working capital isn't a balance sheet line item. It's the operating system underneath your growth. It determines whether you can take the next order, fund the next production run, or pay your suppliers without reaching for equity you can't afford to give up.

If you're building physical products (manufacturing components, fulfilling contracts, sourcing across complex supply chains) working capital management is the difference between a company that scales and one that stalls with a full order book.

The Full Definition: What Working Capital Actually Measures

The standard formula: Working Capital = Current Assets − Current Liabilities

Current assets include cash, inventory, and accounts receivable (money customers owe you for goods already delivered). Current liabilities include short-term debt, accrued expenses, and accounts payable (money you owe suppliers for goods purchased on credit).

The result is either positive or negative.

- Positive working capital means your liquid assets exceed your near-term obligations. You have room to operate, invest, and grow.

- Negative working capital means your short-term liabilities exceed your available resources. You have more coming due than you have available — and that gap has to come from somewhere.

The formula tells you where you stand. What it doesn't tell you is how fast things are moving — or where the pressure is building.

Why Working Capital is Different for Physical-Product Companies

Most working capital guides are written for software businesses. They gloss over the part that kills physical-product companies.

If you manufacture, assemble, or source goods, you carry inventory. And inventory creates timing mismatches that software companies simply don't face. You buy raw materials. You manufacture or source finished goods. You store them. You ship them. And only after all of that do you get paid.

The gap between spending cash and collecting cash is where working capital pressure lives.

At Klear, we work with manufacturers, defense suppliers, and industrial companies, and government contractors everyday. The single most common pattern we see: a founder who is winning contracts and still feels cash-poor. Revenue is growing. The bank account isn't. The cause is almost always a working capital gap hiding inside a healthy P&L.

Your business is not broken, that gap is structural. It's a sign your financing hasn't caught up to how your business actually operates.

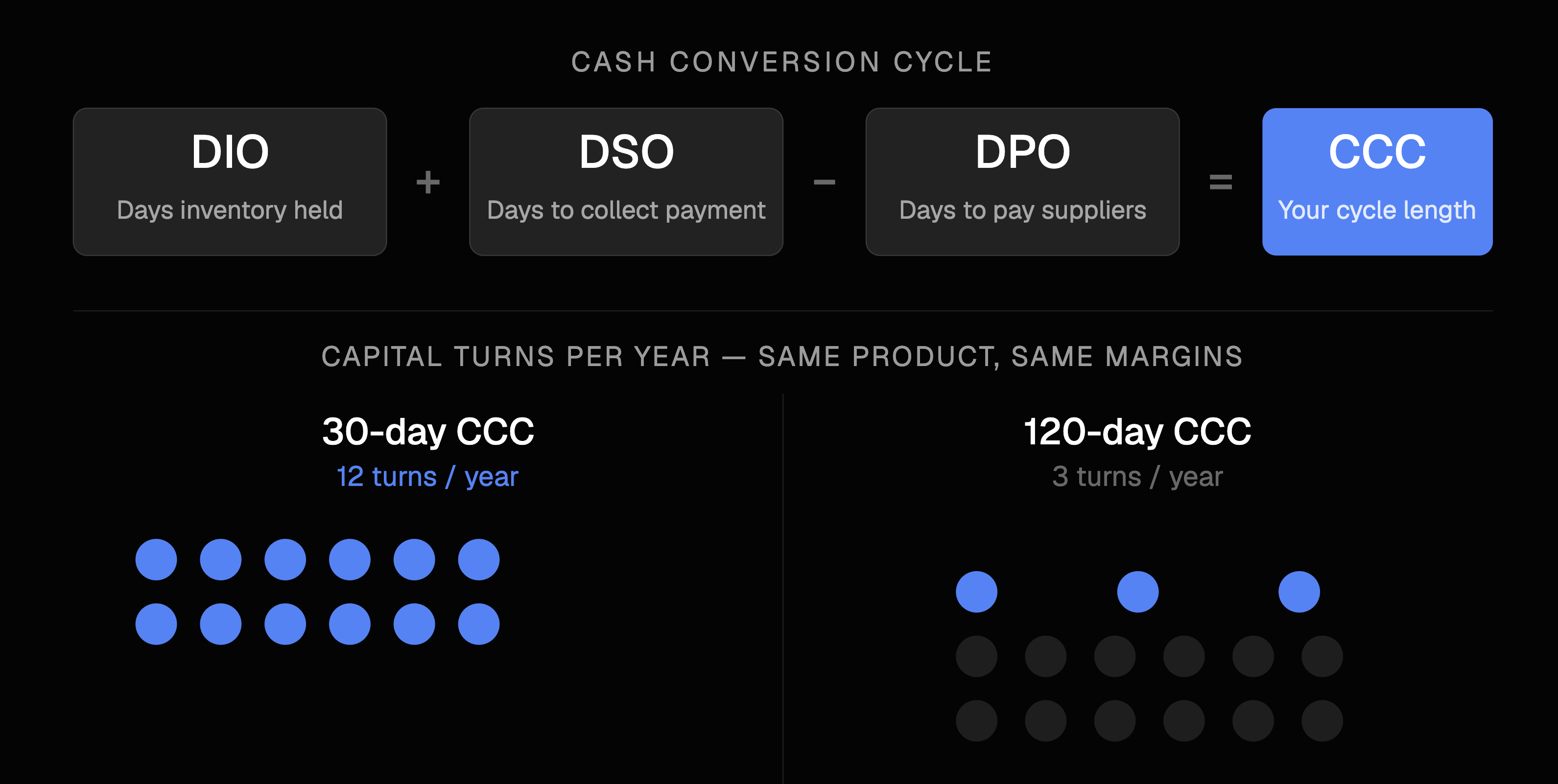

The Cash Conversion Cycle: Your Most Important Metric

The operational expression of working capital is the Cash Conversion Cycle (CCC) the time between when you spend cash and when you get it back.

CCC = Days Inventory Outstanding + Days Sales Outstanding − Days Payable Outstanding

- DIO (Days Inventory Outstanding): how long you hold inventory before selling it

- DSO (Days Sales Outstanding): how long it takes to collect payment after a sale

- DPO (Days Payable Outstanding): how long you take to pay your suppliers

A shorter CCC means cash returns faster, which means you can reinvest, hire, and grow faster.

Here's the math that matters: a company with a 30-day CCC can reinvest its capital 12 times a year. A company with a 120-day CCC gets 3 turns. Same product. Same margins. Completely different trajectory. We call this Capital Velocity, and it's the single biggest lever available to industrial companies that aren't using equity or expensive debt to fund growth.

A defense supplier we work with was sitting on a $4M backlog they couldn't fulfill. Not because they lacked orders. Because their working capital was trapped in invoices waiting to be paid. Unlocking that receivables cycle doubled their effective capacity without a dollar of new equity.

There's also a structural problem worth naming directly: large enterprises optimize their own CCC by extending payment terms to suppliers. Net-60, Net-90, even Net-120 are standard in aerospace and defense. Those terms are someone's asset and someone else's problem.

For the Tier 2 or Tier 3 supplier at the end of that chain, the working capital burden gets pushed onto the companies least equipped to carry it.

Signs Your Working Capital Is Under Stress

These are the patterns we hear from operators before they come to Klear. If any of these sound familiar, the problem isn't your business model, it's your capital structure:

- You're winning contracts but feeling cash-poor. Profitable on paper, worried about payroll in practice.

- You're hesitating on large orders because you're not sure you can fund production.

- Your backlog is building but you can't work through it at the pace demand warrants.

- Sales wants to take more orders. Finance is pumping the brakes.

- You're covering cash shortfalls by selling equity, diluting the cap table to fund operations that should be financed by the work itself.

How to Improve Working Capital: Start With Your Order-to-Cash Cycle

Most working capital guides hand you the same three levers: collect faster, pay slower, reduce inventory… And leave you to figure out the rest. That advice isn't wrong. But it skips the step that actually makes the other three work.

You cannot compress what you cannot see.

The operational expression of working capital isn't a formula. It's your Order-to-Cash cycle: every step from the moment a customer places an order to the moment payment clears. Order management, fulfillment, billing, payment processing. Every handoff, every delay, every gap between those steps is a place where working capital gets trapped — and for most scaling manufacturers, that cycle is spread across disconnected spreadsheets, siloed systems, and email threads between sales and finance.

When the data doesn't talk to each other, neither do your decisions. Sales wants to take the order. Finance isn't sure you can fund it. The backlog builds. The gap between when you need cash and when you receive it widens — and you start bridging it with equity you can't afford to give up.

The fix isn't a faster invoicing process, but a clear map of your O2C cycle with your capital plan built around it.

Operators who can see their inflows and outflows on a single timeline — planned versus actual, across every open order — make fundamentally different decisions than operators who can't. They know where working capital is sitting. They know when it will convert. They can say yes to the next order because they can see the cycle, not just feel it.

This is what Klear's Capital Intelligence™ platform does.

Your team documents purchase orders, invoices, and milestones as part of normal operations. Klear surfaces the intelligence underneath that data: where capital is, where it's going, and where gaps will open before they become emergencies. The result is a repeatable system for managing working capital as your business scales. Not a one-time fix, but a live view of your O2C cycle that gets more useful as order volume grows.

The financing connects directly to that visibility. Working capital that scales with your order book, underwritten against the quality of your customer base rather than the size of your balance sheet. For companies selling to F1000 buyers and government customers, that distinction matters enormously. The strength of your customer relationships becomes the asset, and capital capacity grows as your order book does.

Cakeboxx got to 6x growth and profitability in year one not by optimizing their invoicing process, but by getting a clear picture of their working capital cycle and accessing capital already sitting in their order book. The working capital was there. They needed a system to see it.

Working Capital Is a Growth Strategy, Not a Finance Problem

The founders and operators who understand working capital and actively manage their CCC, align their financing with their order cycles, and treat capital velocity as a strategic lever. Allowing them to scale faster, dilute less, and survive the cash flow shocks that end otherwise great companies.

Working capital management isn't the finance team's job. It's the operating system the whole business runs on.

If you're a manufacturer, a defense supplier, or an industrial company sitting on a growing backlog with capital trapped in invoices, you don't have a growth problem. You have a capital velocity problem… And it's solvable with Klear.

Talk to the Klear team to see how embedded invoice financing can unlock the working capital already in your business.